[♙] Bretton Woods III

The foundations of Bretton Woods II crumbled last week when the G7 seized Russia’s foreign exchange reserves.

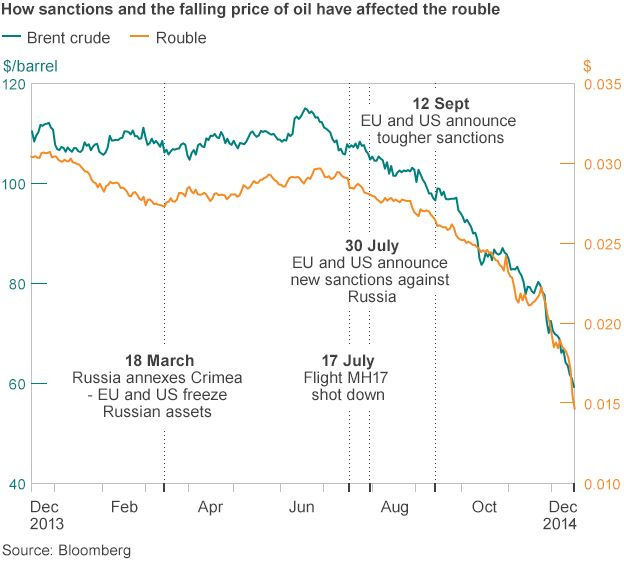

"The U.S. is in a commodity crisis that is giving rise to a new world monetary order that will ultimately weaken the current dollar-based system and lead to higher inflation in the West." - Zoltan Poscar 1

Western sanctions on Russia are likely to cause a paradigm shift in the way the world organizes money and reserves, a “Bretton Woods III” kind of scenario.

Current Era: March 14th 2022

The end of the current US monetary regime occurred the day the G7 nations seized Russia's foreign exchange reserves following the latter's special operation of Ukraine.

The current Ukraine situation delves back to the Minsk agreement - named after the capital of Belarus where they were signed in 2014 and 2015 - in an attempt to secure a ceasefire between the Ukrainian government and Russia-backed separatists in Eastern Ukraine. In the subsequent years, it paved a roadmap for local elections in the occupied regions on Luhansk and Donetsk for independence.

The Ukrainian government views the Minsk agreement as a means to reunite Ukraine, its borders drawn up only in recent times by the USSR, whilst the Kremlin believes that the accords enshrine a process in recognition of the 'Donetsk People's Republic' and 'Luhansk People's Republic' as independent states, thus accorded special status.

Incidentally, “Ukraine’s NATO membership was never “imminent” and will not be on the agenda in the near future” NATO Secretary-General Jens Stoltenberg 2 clarified at a panel discussing the ''Price of peace or cost of war'' organised by the Antalya Diplomacy Forum

[Россия] The Impact Upon Russia

Regarding the effect of Western sanctions, Russian government officials said its economy is in “shock” after heavy sanctions and after a number of Western corporations pulled out of the country in recent days after the Ukraine conflict.

As a main loophole, Russia may still receive dollar payments for oil and natural gas. Russia can also transact outside the SWIFT messaging system via the Chinese and other banks that have not joined the sanctions.

“Our economy is experiencing a shock impact now and there are negative consequences; they will be minimized. This is absolutely unprecedented. The economic war that has started against our country has never taken place before. So it is very hard to forecast anything” said Kremlin spokesman Dmitry Peskov

In response, the Central Bank of Russia imposed capital controls so that Russian companies do not pay interest or principal on international debts, including paying their creditors - in dollars or euros.

Western banks will therefore shrink balance sheets in order to reduce risk, with interbank lending drying up. Inadvertent defaults will compound. These all could trigger a global liquidity crisis.

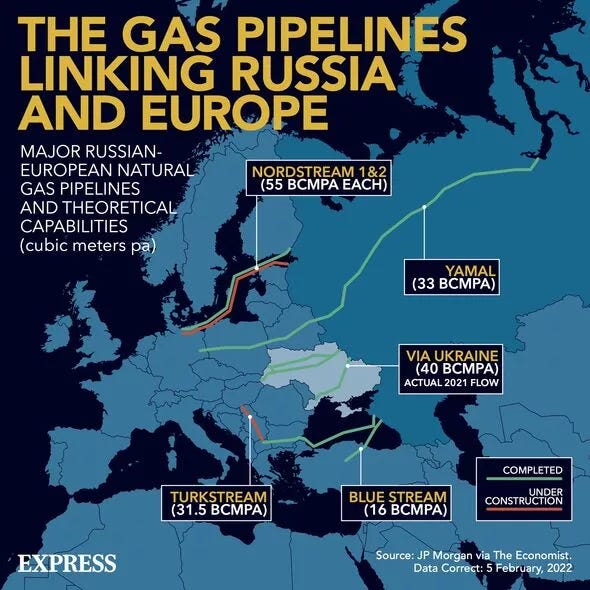

There will also be a ban on the export of certain goods and raw materials outside the country by the end of 2022 - most likely these will be strategic resources such as wheat, fertilizer and precious metals used in industrial production such as aluminum, titanium, palladium, platinum, nickel, cobalt and copper.

Lastly, the impact of higher fertilizer prices has direct impact upon feed grains for livestock, thus resulting in even higher inflation of meat, poultry, eggs and dairy products.

[WEF] The “Great Reset” Narrative

SWIFT was built as a financial messaging system to support global commerce.

However the U.S. Biden-led sanctions, de-swifting and confiscation of personal assets of Russians and foreign reserves effectively ends the current global economy resulting in a massive monetary-economical waterfall crisis.

And thus, ironically the US has sealed the fate of the USD itself and made inherently apparent, the alternatives to the US/Eurodallar SWIFT paradigm - or by design.

To align with the WEF narrative of a “great reset”, the role of USD as world reserve currency has to collapse to allow for a new digital world currency.

Ordo ab Chao

A Fourth Turning 3, realigning the NATO/Europe/Russia/China axis has truly arrived - a generational era of destruction, involving global revolution, in which institutional life is destroyed and rebuilt in response to a perceived threat to the nation's survival. Described as a four-stage cycle of social eras aka "turnings" by Strauss & Howe.

The turnings include: "The High", "The Awakening", "The Unraveling" and "The Crisis". Each generational turning lasts about 20–22 years. The “Four turnings” make up a full cycle of about 80 to 90 years.

Each of these turnings can be described as the "seasons of history", with each Fourth Turning describing a distinct mood that recurs every saeculum.

Generational change drives these cycle of turnings and determine its periodicity. As each generation ages into the next life phase (and a new social role) society's mood and behavior fundamentally changes, giving rise to a new turning.

The First Turning is a High, which occurs after a Crisis.

In the US, this was the post–World War II American High, beginning in 1946 and ending with the assassination of John F. Kennedy on November 22, 1963.The Second Turning is an Awakening, whereby institutions are attacked in the name of personal and spiritual autonomy. People tire of social discipline and want to recapture a sense of "self-awareness", "spirituality" and "personal authenticity".

The US's most recent Awakening was the "Consciousness Revolution," which spanned from the campus and inner-city revolts of the mid-1960s to the tax revolts of the early 1980s.The Third Turning is an Unraveling, whereby Institutions are weak and distrusted, whilst individualism is strong and flourishing.

Highs come after Crises, when society wants to coalesce and build and avoid the death and destruction of the previous crisis. Unravelings come after Awakenings, when society wants to atomize and enjoy.

The most recent Unraveling in the US began in the 1980s and includes the Long Boom and Culture War.The Fourth Turning is a Crisis.

This is an era of destruction, often involving war or revolution, in which institutional life is destroyed and rebuilt in response to a perceived threat to the nation's survival. After the crisis, civic authority revives, cultural expression redirects towards community purpose, and people begin to locate themselves as members of a larger group.

The previous Fourth Turning in the US began with the Wall Street Crash of 1929 and climaxed with the end of World War II. The G.I. Generation (Hero archetype, born 1901 to 1924) came of age during this era - epitomised by confidence, optimism, and collective outlook mood of that era.

The Millennial Generation (Hero archetype, born 1982 to 2004) show many similar traits to those of the G.I. youth, epitomised by rising civic engagement, improving behavior, and collective confidence

Framed within the context of turnings, the erosion of trust between Russia and the West has brought us to the brink of a conflict that could have far reaching consequences for Europe, a restructuring of the Bretton Woods II and global monetary system and ushering a multipolar realignment

It could be the intentional provocation and egging on of Ukraine with the coy suggestion of membership consideration into EU and NATO has led to the inevitable current crisis - viewed as an opportunity for the US and its NATO allies to “exacerbate” tensions in order to weaken Putin.

With Biden repeatedly whipping up MSM stories of a imminent Russian invasion, there was a distinct “wag the dog” scenario playing out the week prior to February 24th special military operations by the Russian Armed Forces, preceeded by a massive military strategic positioning and joint military exercise “Union Courage-2022” upon the Belarusian-Ukraine borders on February 10th.

And upon that fateful day, at 06:00 Moscow time 24th February 2022 (06.6.II.6) - Putin announced a "special military operation" in eastern Ukraine, in order to protect people "who have been suffering from abuse and genocide by the Kiev regime for eight years."

There may be trouble ahead.

[СПФС] Alternatives to USD/SWIFT Paradigm

Russia & China have had a decade to prepare for such, with the SPFS 4 and CIPS 5 frameworks respectively. As such, Russia has built up massive foreign reserves, stockpiled resources and a massive surplus with lower debt of $121 billion to foreign instituitions in comparison to U.S. $33 trillion debt 6.

In actuality, the U.S and the Atlantic backers stands to benefit most from the Ukraine situation.

That said, “the sanctions will still hurt the Russian people to some degree (and the oligarchs not so much). And the Russian government will not take kindly to this damage, even if it will be far more limited in scale” as opposed to the scenario being presented by the MSM - as financial analyst J. Kim notes astutely in his latest skwealthacademy substack:Will Russian Gold Sanctions Finally Reveal that The Emperor Has No Clothes?

Speculatively, the net effect of all these market forces could be for greater adoption of Decentralised Finance and some sort of stablecoin adoption, with investors fleeing towards safe havens (energy and precious metals) amidst the market volatility, depression of pandemic stocks, knock on effects of global supply chains and food, nitrogen, semi conductor and neon shortages.

[ ₿ ] Effect of Ukraine on Cryptocurrency

The Bitcoin price remains flat at around $39k, with other major cryptocurrencies seeing similar movements, Ethereum hovers at just above $2,500.

On Monday the European Parliament's economic and monetary affairs committee voted 30-23 not to take forward an amended version of Markets in Crypto Assets (MiCA) 7requiring all currency providers to submit detailed proposals about how they would comply with environmental sustainability standards

To reduce the cryptos' carbon footprint, MEPs have asked the European Commission to include crypto-assets mining in the EU taxonomy (a classification system) for sustainable activities by 2025.

The most-recent draft of the European Union’s (EU) proposed legislative framework for governing virtual currencies, had originally a proposed ban on the proof-of-work (PoW) mechanism that Bitcoin and several other major cryptocurrencies use to confirm transactions.

Instead, a more mild version of the bill will continue its legislative journey. It states that by January 1 2025, the European Commission shall present a new proposal “with a view to including in the EU sustainable finance taxonomy any crypto-asset mining activities that contribute substantially to climate change mitigation and adaption”.

Crypto-assets are neither issued nor guaranteed by a central bank or a public authority and are therefore currently out of the scope of EU legislation.

The European Parliament argues this can cause "risks for consumer protection and financial stability" and could lead to market manipulation and financial crime.

To appreciate the meta narrative, that encompasses both geo economics, world power and collateral, Investment Strategist Zoltan Pozsar (Global Head of Short-Term Interest Rate Strategy, Credit Suisse) frames it as thus: “A crisis is unfolding. A crisis of commodities. Commodities are collateral, and collateral is money, and this crisis is about the rising allure of outside money over inside money.”

The initial Bretton Woods era (1944-1971) was backed by gold

Bretton Woods II (1971-present) was backed by "inside money" (essentially U.S. government paper)

Bretton Woods III will be backed by "outside money" (gold and other commodities)

[] De-SWIFT Fallout

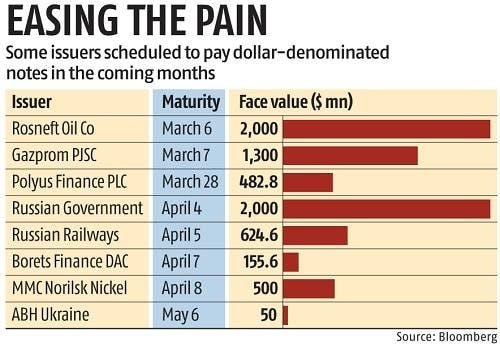

International banks are owed roughly $121 billion8 by Russia-linked entities, according to data from the Bank for International Settlements—and because of the recent decoupling of the West and Russia, clients are unlikely to recover most of that money back.

"BlackRock will continue actively consulting with regulators, index providers, and other market participants to help ensure our clients can exit their positions in Russian securities, whenever and wherever regulatory and market conditions allow."

BlackRock’s clients held around $18.2 billion in exposure to Russia-linked assets with the total exposure of their clients to Russian securities representing just 0.18% of their total assets under management a month ago (Feb 22’) and has dropped to less than 0.01% of current client assets.

As banks across the U.S. are forced to divest from Russian firms amid regulatory and licensing restrictions brought about by strict Western sanctions, Russian President Vladimir Putin also gave his country’s financial institutions permission to seize assets left behind by Western companies.

“If foreign owners close the company unreasonably, then, in such cases, the government proposes to introduce external administration. Depending on the decision of the owner, it will determine the future fate of the enterprise.”

Russian Prime Minister Mikhail Mishustin said in a statement.

—[ ℳonetary $¥$₮€₼₪ + ₿ In Review ]—

[] SFPS & CIPS

Russia & China share a multi-polar strategic relationship; albeit China is more important to Russia

The reality is Russia’s development of its SFPS (System for Transfer of Financial Messages), which has a sister in China known as the CIPS (Cross-Border Interbank Payment System), the “de-SWIFTing” of Russia by the Belgium entity will not have nearly the devastating consequences as being projected by the Western mass media.

More than a decade ago, Chinese officials had stated a strong need to expedite the development of their SWIFT-alternative CIPS system to prepare them for their inevitable de-SWIFTing.

The Cross-Border Interbank Payment Systems (CIPS) is a Chinese government payment system specializing in facilitating cross-border payments denominated in the renminbi (RMB). CIPS operates in more than 100 jurisdictions around the world, with about half of the participants located in China. CIPS relies on SWIFT’s messaging services to access SWIFT’s large network, although CIPS is reportedly developing the means to eventually operate independently from SWIFT.

Russia’s System for Transfer of Financial Messages (SPFS), launched in 2014 in response to U.S. and EU sanctions imposed on some trade with and investment in Russia because of its invasion of neighboring Ukraine, has been marketed as a direct alternative to SWIFT for financial messaging.

“If China knew this day would come more than a decade ago, surely Russia knew back then as well.”

As such, it is far more realistic “to believe that Russia’s more than decade long preparation for such a response had adequately prepared it to handle the pro-USD, anti-gold banking cartel’s de-SWIFTing of Russia without many glitches.”

Therefore, the Russian government will be likely to respond strongly to such sanctions, even if the scale of damage is limited. And the Russian response to economic sanctions will be the key to the possibility of the curtain on Western banking cartel fraud being revelaed to be backed by… nothing i.e. wherby the proverbial Fort Knox has long been depleted due to massive overleveraged re-hypothecation of gold.

Crypto and BTC: Opportunities Abound

Bitcoin represents a rework of monetary trade as a rules based monetary system.

Its benefits are rapid instantanous transaction, tamper proof verification using an an open ledger, not controlled by any state or corporation. It has a fixed supply of scarcity of 21 million units as a store of value. BTC currently has a market value of $8 trillion, with a hedge against inflation or deflation.

Bitcoin solves multiple challenges of Money without neccesating a intermdieary such as a state.

Store of value (high value)

Means of exchange (transcation)

Unit of Account (reserve currency)

Bitcoin has merit to solve at its base layer as a store of value.

A day to day transaction could involve a second layer via exchanges such as Lightning. As latency decreases with high connectivity at low cost, your base layer could perform multiple scalar transactions eg BTC and ETH.

Modern finances eg. credit cards, ACH and wire transfers operate on a relatively an archaic network of information systems, which is unsecured and slow (much akin to data transfer, with a visible username and password) which may take 1-2 days to reconcile using batch procssing with potential for error.

The flipside of such reliance of such technologies reliant on mobile apps, smart contracts and digital only transations: in a unexpected event, loss of power and energy - such digital value is essentially worthless very much like a book does not require electricity to be powered on, a hard wallet is only as good as a reliable transfer of perceived value between peers as a convenient secure form of wealth trsanfer.

[] All That Is Gold & Silver

As a small aside, one needs to look at the curious case of precious metals

The gold-silver ratio is the oldest continuously tracked exchange rate in recent history.

The Roman Empire officially set the ratio of Gold to Silver at 12:1

The ratio reached 14.2:1 in Venice in 1305 and remained at this level up until 1330 when it fell to 10:1. It climbed back to 12:1 in the 1450s.

The U.S. government fixed the ratio at 15:1 with the Coinage Act of 1792

Subsequently, President Roosevelt set the price of gold at $35 an ounce in 1934, with a masssive inflation of the ratio of 98:1 in 1939.

Following the end of World War II, and the Bretton Woods Agreement of 1944, foreign exchange rates were pegged to the price of gold.

The Bretton Woods Agreement also created two monetary cartels based in Washington, D.C — the International Monetary Fund (IMF) and the World Bank.

Functionally, the IMF oversees the stability of the world's monetary system, whilst the World Bank’s aims are to project soft power via offering assistance to middle-income and low-income countries (in lieu of providing financing, advice, and research to developing nations to aid their economic advancement)

The World Bank’s main flagship is the Human Capital Index (HCI) - used to identify what is lost from the lack of investments in human capital and how to remedy these deficiencies. Its other goals measure the effectiveness of a nation's educational and healthcare systems; affecting policy, mandates & insight on where to allocate resource using a "whole government" approach to addressing factors that compromise human capital (as a critical monetary productive resource).

The Bretton Woods Agreement was negotiated in July 1944 by 730 delegates representing 44 countries at the United Nations Monetary and Financial Conference held in Bretton Woods, New Hampshire. The new world financial cartel had its principal goals of creating an efficient foreign exchange system, preventing competitive devaluations of currencies, and promoting international economic growth

Under the Bretton Woods System, gold was the basis for the U.S. dollar and other currencies were pegged to the U.S. dollar’s value. The Bretton Woods System effectively came to an end in the early 1970s when President Richard M. Nixon announced that the U.S. would no longer exchange gold for U.S. currency.

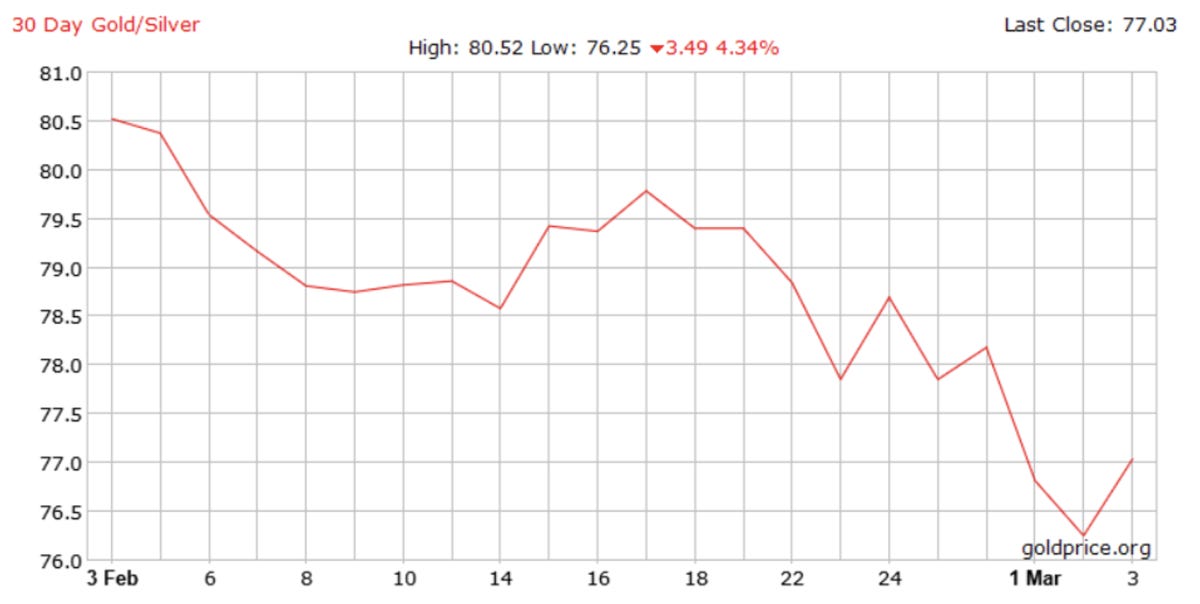

The gold-silver ratio shows the number of ounces of silver it takes to equal the value of one ounce of gold. For example, if the price of gold is $1,000 an ounce and the price of silver is $20 an ounce, then the gold-silver ratio is 50:1

During the 20th century, the average gold-silver price ratio was 47:1, and has since increased to 85:1, 60% above 20 year average ratio of 60:1.

[] The Impact of Ukraine on the Gold/Silver Ratio

Fast forward to the impact on global 2022 monetary volatility, silver futures (SI) have gained ground over the last week or so but are still more than ten percent below the 52-week high. By contrast, gold has soared to its highest levels for a couple of years and is less than seven percent below its all-time high.

[] QE Infinity and Beyond

Markets Awaits Fed Rate Hike Wednesday

Within the short term, the decision to take some lenders off SWIFT might neccesitate further FED involvement amidst the extreme volatility.

Next week’s money options expiry will be the biggest concentration since 2019. How dynamic will the situation play out considering the Russian/Ukraine situation, the renewed China bear and the Fed event.

The FED certainly faces a policy dilemma of its own design - the FOMC is widely expected to announce this day a 0.25% rate hike, the first of seven rate hikes for several years (with a small chance that the hike will be double that size, at 0.50%). The markets are certainly expecting rate hikes by July 2022 totalling 1.00%, so Wednesday’s hike is just the start. Even if it is a 0.50% rate hike, there will almost certainly be two more hikes before the third quarter.

Cui Prodest? ("whom does it profit?")

The US Dollar is the strongest of all major currencies, and closed Friday at a 5-year high price against the Japanese Yen.

The US Dollar is strengthened due a regime of expected rate hikes and the Dollar has been boosted as a safe haven during the current period of geopolitical crisis resulting from the Russian invasion of Ukraine.

"It is also worth noting that US inflation is now rising at an annualized rate of 7.9%, a 40-year high, and will likely be even higher next month when the impact of recent commodity price rises begins to filter through into the latest CPI data.”

This is likely to further reinforce the case for more hawkish policy action from the Fed.

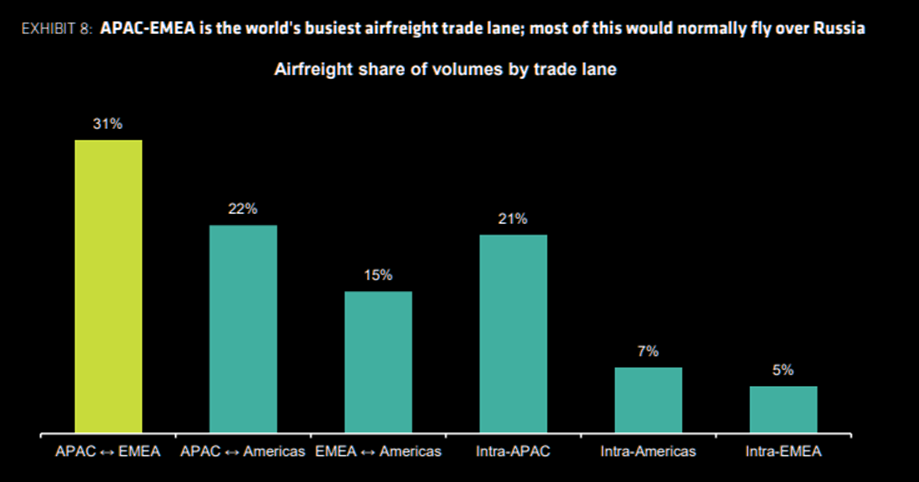

Logistics wise, 20% of global air freight moves between Europe and Asia, leading to international supply chains disruptions due to lack of overflight in Russian airspace. 3% of the current Asia-Europe ocean demand passes thru Russia via the China-Europe rail link , whilst the impact via shipping lines thru Russian ports is minimal, accounting for just 1% of ocean container throughput.

[] TIMELINE | NATO/ОДКБ / spec ops

10th Feb - 14th March 2022

[] 10th Feb 22 | UNION COURAGE - 2022

The joint military exercise “Union Courage-2022” was organized by Russia and Belarus near the borders of NATO and Ukraine, and began on 10 February in Belarus

The exercises were held in five training grounds in Belarus’ west and south-west, namely Domanovsky, Gozhsky, Obuz-Lesnovsky, Brest, and Osipovichsky including four airfields: Baranovichi, Luninets, Lida, and Machulishchi.

Troop deployments: Russia reported that troops from Siberia and the Eastern Military Region were sent to Belarus for the exercise, which has been in the works for nearly a month.

Su-35 fighters, Su-25SM attack aircraft, S-400 air defense systems and Pantsir-S systems were also deployed for the exercises, in which an estimated 30,000 Russian soldiers are set to participate. Additionally, sources indicated Russia had deployed Iskander-M ballistic missile systems capable of carrying nuclear warheads to Belarus.

In response, Ukrainian President Volodymyr Zelensky stated, “the accumulation of forces near the border is psychological pressure from our neighbors.”

The Ukrainian government, on the other hand, is kicking off a 10-day military exercise with unmanned aircraft and anti-tank missiles today. Ukrainian Defense Minister Oleksiy Reznikov declared that from 10–20 February, his country would conduct a parallel exercise to improve the Ukrainian armed forces’ readiness.

[] 24th Feb 22 | SPECIAL MIL OPERATIONS

[24/2/2022] 06.6.II.6

At 06:00 Moscow time, Putin announced a "special military operation" in eastern Ukraine, in order to protect people "who have been suffering from abuse and genocide by the Kiev regime for eight years."

It represents the largest conventional military attack in Europe since World War II.

Russian Armed Forces carried out a precision cruise missile strike via air-and naval-based cruise missiles on 800 Ukrainian military infrastructure objects.

"Russian Armed Forces hit a total of 821 Ukrainian military infrastructure objects, including 14 military airstrips, 19 control centers and communication nodes, 24 S-300 and Osa missile air defense systems, 48 radar stations"

[5th March] 2,119 military targets (911-II.0)

The Russian leader stressed that Moscow had no plans of occupying Ukrainian territories. The goal is demilitarization and denazification of that countr - limited to surgically striking and incapacitating Ukrainian military infrastructure

"A total of 2,119 targets of Ukraine’s military infrastructure have been hit during the operation. Among them are 74 command posts and communication points of the Ukrainian Armed Forces; 108 air defense missile systems of S-300, Buk-M1 and Osa, as well as 68 radar stations"

The Key Strategic Targets

Одеса - known as the "pearl of the Black Sea". In 1794, the city of Odessa was founded by a decree of the Russian empress Catherine the Great.

Чорнобиль | Chernobyl Exclusion Zone 9

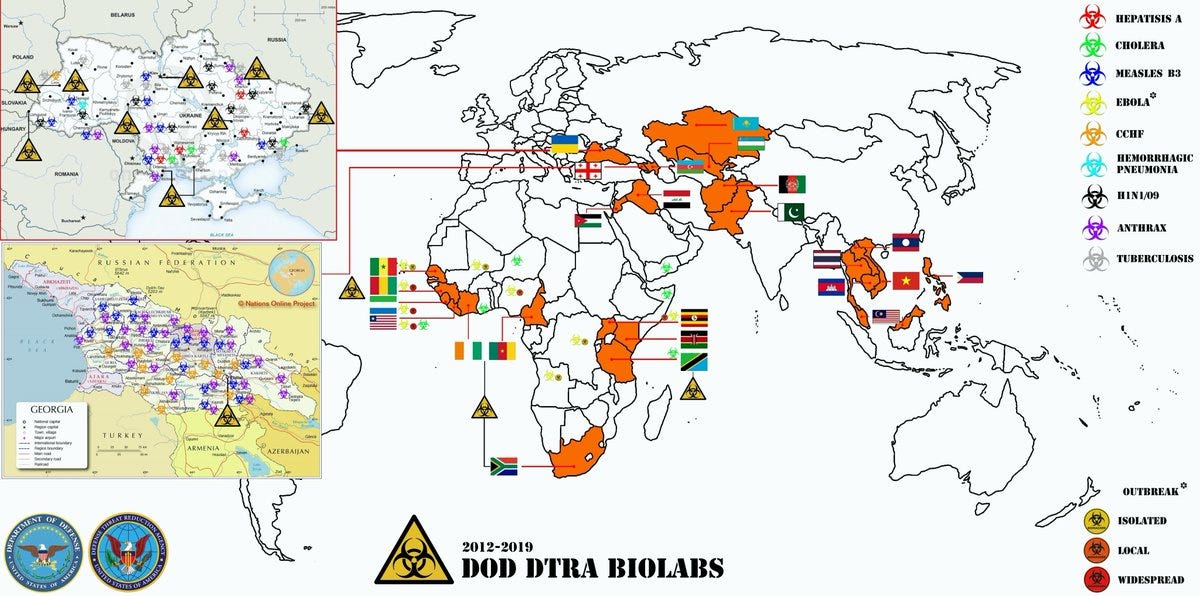

40 strategic DoD-Ukrainian BTRP funded biolabs 10

[] 11th March 22 | US & EU SANCTIONS

Joe Biden bans Russian oil imports

On Tuesday, 8th March President Joe Biden announced the United States would ban all Russian oil imports, raising the likelihood of soaring gas prices domestically, over the Ukraine war. And on Wednesday 9th March, the European Union announced that it would expand its sanctions on both Russia and Belarus

[] 12th March 22 | DAY 17

Ukrainian troops stand behind a barricade in front of the Odesa National Academic Theatre of Opera and Ballet

Meanwhile, “there are reports of looting and violent confrontations among civilians over what little basic supplies remain in the city” in the besieged southern city of Mariupol

[] 12th March 22 | ISRAELI PM MEDIATES

Ukrainian defense official: ”We appreciate Bennett’s mediation”

Over the weekend, Prime Minister Naftali Bennett told Ukrainian President Volodymyr Zelenksy that he recommends Ukraine take the offer made by Russian President Vladimir Putin to end the war (Zelensky and his advisors were infuriated by the recommendation).

As terms of negotiation, the offer Russia has demanded - “that to end the war, Ukraine must recognize Russian sovereignty over Crimea, the statehood of Donetsk and Luhansk, as well as write neutrality regarding NATO into its national constitution, or effectively 'demilitarize' itself vis-a-vis its relationship with the Western military alliance.”

The phone call was initiated by Bennett. "If I were you, I would think about the lives of my people and take the offer," Bennett reportedly said.

Zelenksy's response was short. "I hear you," he said

The Jeruselam Post

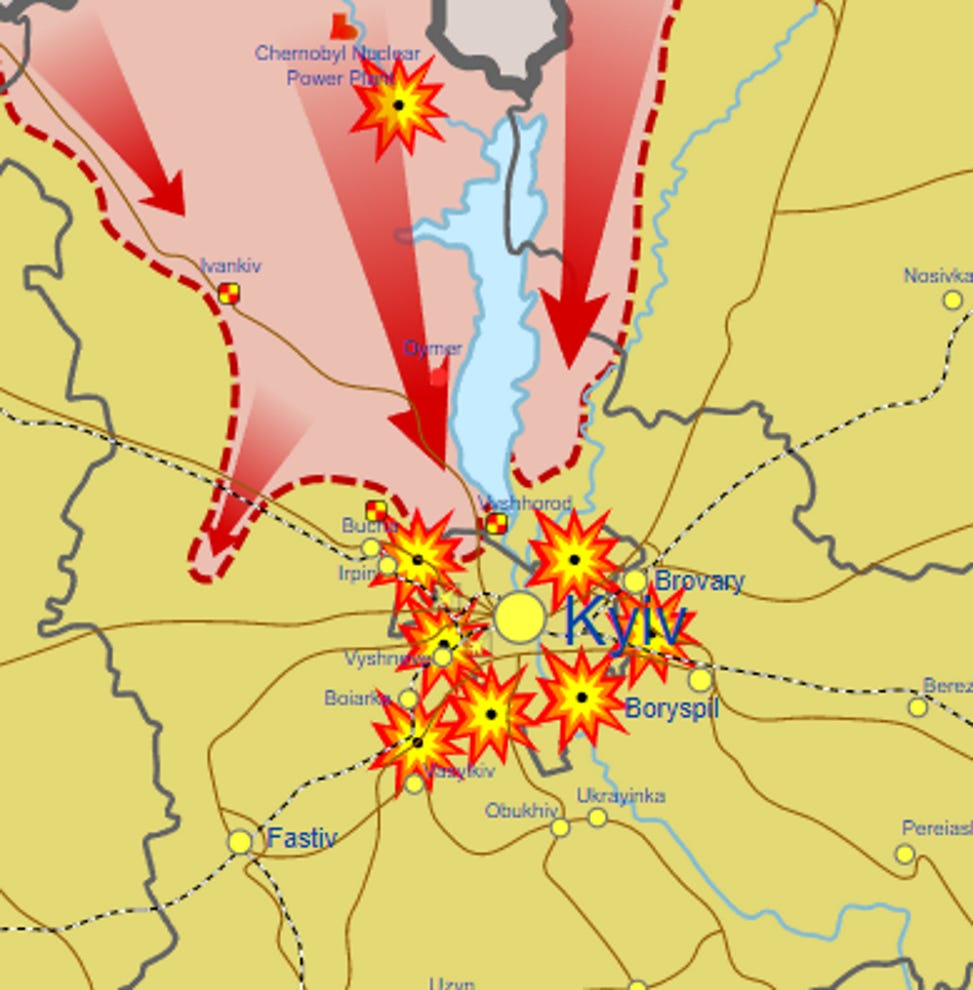

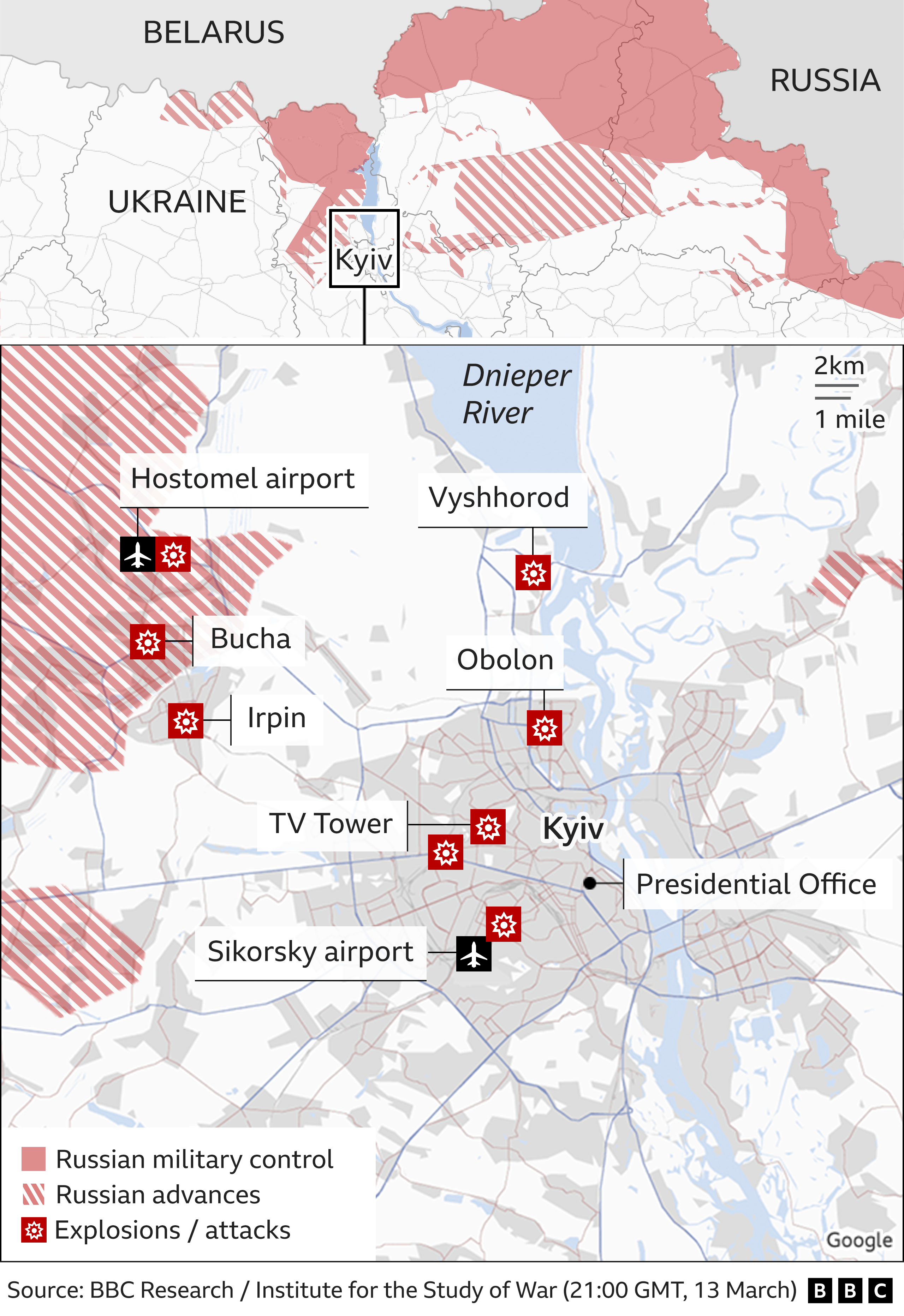

[] 13th March 22 | THE FIGHT FOR KYIV

Russian forces attempt to encircle and cut off the Ukrainian capital, with troops moving towards the city from multiple positions. Russian missiles also targeted a factory which makes Antonov aircraft at Sviatoshyn Airfield, about six miles (10km) from Kyiv city centre.

Russian forces held off attacking north-eastern Kyiv on Sunday, instead focused on reinforcing their lines of communication and logistics routes, according to the Institute for the Study of War (ISW).

The 40-mile Russian armoured column has now dispersed into the area west of Kyiv, moving more artillery and rocket launchers to within range of the capital.

The city is bracing itself for a ground assault, with Ukrainian forces and volunteers building new defences and creating barricades on major routes to slow any Russian attack.

[] 14th March 22 | Western Sanctions

Russia To Pay Foreign Debts In Rubles

Half of Russia’s $643bn foreign reserves had been hit by the sanctions.

Russia’s finance ministry confirmed a temporary procedure for repayment of foreign currency debt was in place, but warned payments would be made in rubles if debts could not be honoured in the currency of issue due to bank sanctions.

Russia can still access about half of its foreign reserves, which are held in currencies like the Chinese yuan or in assets like gold. Siluanov on Sunday expressed hope that Russia could expand its yuan holdings, which currently make up 13% of its total reserves, as China has so far said it would "not participate" in sanctions against Russia.

Anton Siluanov, Russia’s finance minister said that, it was “absolutely fair” the country would make all of its sovereign debt payments in roubles so long as sanctions that have frozen $300bn of the country’s reserves remain in effect, Russia would use rubles to pay back its debt—even if the debt is owed in foreign currency.

“We need to pay for critical imports. Food, medicine, a whole array of other vital goods. But the debts we need to pay to the countries that have been unfriendly to the Russian Federation and have limited our use of foreign currency reserves — we will pay off our debt to these countries in the rouble equivalent,”

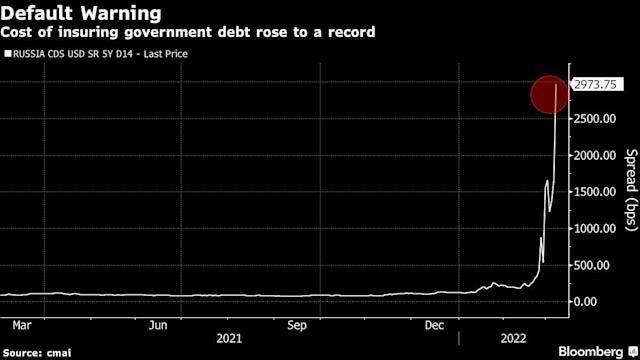

Russia is scheduled to pay $117 million on two dollar-denominated bonds on 16th March. It has a 30-day grace period to make a payment before it is technically in default. The bond does not allow Russia to pay its obligations in rubles, which means Russia's promise to pay back debts in rubles would still trigger a default. 11

The international finance sector is bracing for such an event, which would mark Russia's first default on debt since 1998, and its first on foreign-held debt since 1917. Fitch downgraded its rating for Russian government bonds to its second-lowest level last week, saying that a Russian debt default was “imminent”. Moody’s and S&P have also downgraded their ratings of Russian bonds to junk status.

Russia's gold hoard, which makes up about $130 billion of its reserves is held in a vault in the Russian central bank.

Footnotes

Credit Suisse Economics

Breton Woods III by Zoltan Pozsar

212 538 3779 / zoltan.pozsar@credit-suisse.com

We are witnessing the birth of Bretton Woods III – a new world (monetary) order centered around commodity-based currencies in the East that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West.

A crisis is unfolding.

A crisis of commodities.

Commodities are collateral, and collateral is money, and this crisis is about the rising allure of outside money over inside money. Bretton Woods II was built on inside money, and its foundations crumbled a week ago when the G7 seized Russia’s FX reserves...

The beautiful paradox of linear rates (the stuff you trade and I write about) is

that you need to think linear to find relative value most of the time, but you have to think non-linear to recognize and survive regime shifts.

We are seeing a regime shift unfold in funding markets currently (which, as always, will pass), and a sea change in inflation dynamics and FX reserve management practices

We have two convictions today.

First, June FRA-OIS spreads can widen more, to at least 50 bps, both due to funding premiums driven by commodity prices and the market taking out Fed hikes, and second, it’s a good time to get long...

...shipping freight rates. Yes, freight rates, which, at the current juncture are

linked to “geo-monetary” dynamics.

Freight rates are the price of balance sheet for “commodity RV traders” (the commodity trading houses) and for sovereigns that can take the risk of moving and storing subprime, sanctioned commodities.

First, funding.

Since the start of the conflict in Ukraine, spot U.S. dollar Libor, FRA-OIS, and FX swaps have been showing signs of stress. Not much, but we hear two things from funding desks: cash is bid, and term cash is hard to come by.

Normally, where o/n points trade in the FX swap market determines how the rest

of the curve trades (low premia in o/n space mean low premia in term space).

But these aren’t normal times.

We have a crisis of sorts unfolding, and in a crisis, like in 2008, everyone lends at short maturities and the collapse in o/n premia is at the expense of term premia – in a crisis, term funding premia increase on the back of compressed o/n premia, as opposed to decline as they normally would.

Who drives the bid for cash, i.e. whose bid is driving term funding premia in

this environment where lenders are less willing to lend cash for longer tenors?

The commodities world, for three reasons.

First, non-Russian commodities are more expensive due to the sanctions-driven supply shock that basically took Russian commodities “offline”.

If you are a (leveraged) commodities trader, you need to borrow more from banks to buy commodities to move and sell them.

Second, if you are long non-Russian commodities and short the related futures,

you are likely having margin calls that need to be funded.

Anyone in the commodities world is experiencing a perfect storm as correlations suddenly shot to 1, which is never a good thing. But that’s precisely what happens when the West sanctions the single-largest commodity producer of the world, which sells virtually everything. What we are seeing at the 50-year anniversary of the 1973 OPEC supply shock is something similar but substantially worse – the 2022 Russia supply shock, which isn’t driven by the supplier but the consumer.

Third, if you are short Russian commodities and long the related futures, then

you are likely having margin calls too that also need to be funded like above.

The aggressor in the geopolitical arena is being punished by sanctions, and

sanctions-driven commodity price moves threaten financial stability in the West.

Is there enough collateral for margin? Is there enough credit for margin? What

happens to commodities futures exchanges if players fail? Are CCPs bulletproof?

I haven’t seen these topics in the wide offering of Financial Stability Reports,

have you?

Is the OTC commodity derivatives market the gorilla in the room?

The commodities market is much more financialized and leveraged today than

it was during the 1973 OPEC supply crisis, and today’s Russian supply crisis is

much bigger, much more broad-based, and much more correlated. It’s scarier.

The higher non-Russian commodity prices get and the lower Russian commodity prices fall, the wider FRA-OIS will get, and if you want to express all this in the credit space, look at what CDS spreads on some bigger commodity traders have done since we published our Dispatch on commodity derivatives on Friday.

Spot on!

Next, let’s move on to the freight rates and Bretton Woods III angles.

Regular readers of this publication know of Perry Mehrling: my “Keynes” and

father of the money view.

As Perry Mehrling taught me, money has four prices:

(1) Par – which is the price of different types of money and which means

that cash, deposits, and money fund shares should always trade 1:1.

(2) Interest – which is the price of future money and which refers to OIS

and spreads around OIS across all possible money market segments.

(3) Exchange rate – the price of foreign money, i.e. U.S. dollars vs. the rest.

(4) Price level – which is the price of commodities (all of the Russian,

non-Russian stuff) and, via commodities, the price of everything else.

Recall our conversation in Friday’s Dispatch about the parallels between the

currently unfolding crisis and the crises of 1997, 1998, 2008, and 2020, and

the conclusions that we drew from the review of these crises. These were that

every crisis occurs at the intersection of funding and collateral markets and that, in the presently unfolding crisis, commodities are collateral, and more precisely, Russian commodities are like subprime collateral and all other stuff is prime.

Now, back to the four prices of money and how they link up with these themes:

(1) Par – this is what broke in 2008 when money funds broke the buck

and funding markets froze from fearing subprime mortgage collateral.

(2) Interest – this is what broke in 2020 when bond RV trades crashed as

the drawdown of credit lines pulled funding away from good collateral.

(3) Exchange rate – this is what broke in 1997 when collateral (FX reserves)

went missing and U.S. dollar funding staged a sudden stop in Asia.

(4) Price level – this is what’s in play as we speak..

NATO: Antalya Diplomacy Forum - ''Price of peace or cost of war'

NATO Secretary-General Jens Stoltenberg said on Friday, Ukraine’s NATO membership was never “imminent” and will not be on the agenda in the near future.

Speaking at the Antalya Diplomacy Forum, the NATO chief said that “it has been clear for a long time that membership for Ukraine was not something that was imminent, not something which is relevant in the near future."

The Strauss–Howe generational theory, devised by William Strauss and Neil Howe, describes a theorized recurring generation cycle in American history and global history.

According to the theory, historical events are associated with recurring generational personas (archetypes). Each generational persona unleashes a new era (called a turning) lasting around 20–25 years, in which a new social, political, and economic climate (mood) exists. They are part of a larger cyclical "saeculum" (a long human life, which usually spans between 80 and 100 years.

Strauss and Howe laid the groundwork for their theory in their 1991 book Generations, which discusses the history of the United States as a series of generational biographies going back to 1584.

In their 1997 book The Fourth Turning, the authors expanded the theory to focus on a fourfold cycle of generational types and recurring mood eras to describe the history of the United States, including the Thirteen Colonies and their British antecedents. However, the authors have also examined generational trends elsewhere in the world and described similar cycles in several developed countries

SPFS

Система передачи финансовых сообщений (СПФС)

'System for Transfer of Financial Messages') is a Russian equivalent of the SWIFT financial transfer system, developed by the Central Bank of Russia. Since March 2018, there have been over 400 institutions (mostly banks) as part of the network - with transaction fees at 0,80–1,00 ₽ (0.012–0.015 $) per transaction.

The system currently only works within Russia, with plans to integrate the network with the China-based Cross-Border Inter-Bank Payments System.

At the end of 2020, there were 23 foreign banks connected to the SPFS from Armenia, Belarus, Germany, Kazakhstan, Kyrgyzstan and Switzerland. The Russian Government is also in talks to expand SPFS to developing countries such as Turkey and Iran

CIPS

https://crsreports.congress.gov/product/pdf/R/R46843

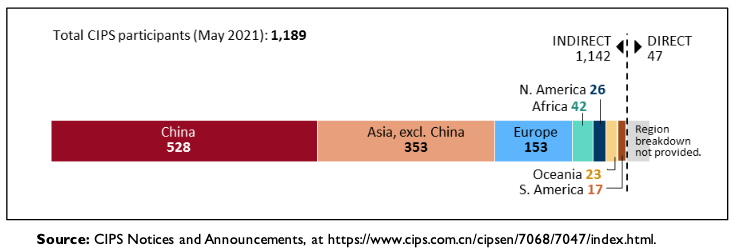

The Cross-Border Interbank Payment Systems (CIPS) is a Chinese-government payment system specializing in facilitating cross-border payments denominated in China’s national currency, the renminbi (RMB).

The China International Payment Service Corporation (CIPS Corp.), is controlled and run by China’s central bank, People’s Bank of China (PBOC). Financial institutions using CIPS are categorized as direct or indirect participants: direct participants hold an account with CIPS and can send or receive messages directly in the system, while indirect participants gain access to CIPS through direct participants.

CIPS operates in more than 100 jurisdictions around the world, with about half of the participants located in China. As of May 2021, CIPS has a total of 1,189 participants (47 direct and 1,142 indirect). It was launched on October 8, 2015, to support cross-border trade, financing, and investment as part of the Chinese government’s effort to internationalize the RMB.

CIPS collaborates closely with SWIFT. CIPS relies on SWIFT’s messaging services to access SWIFT’s large network, although CIPS is reportedly developing the means to eventually operate independently from SWIFT

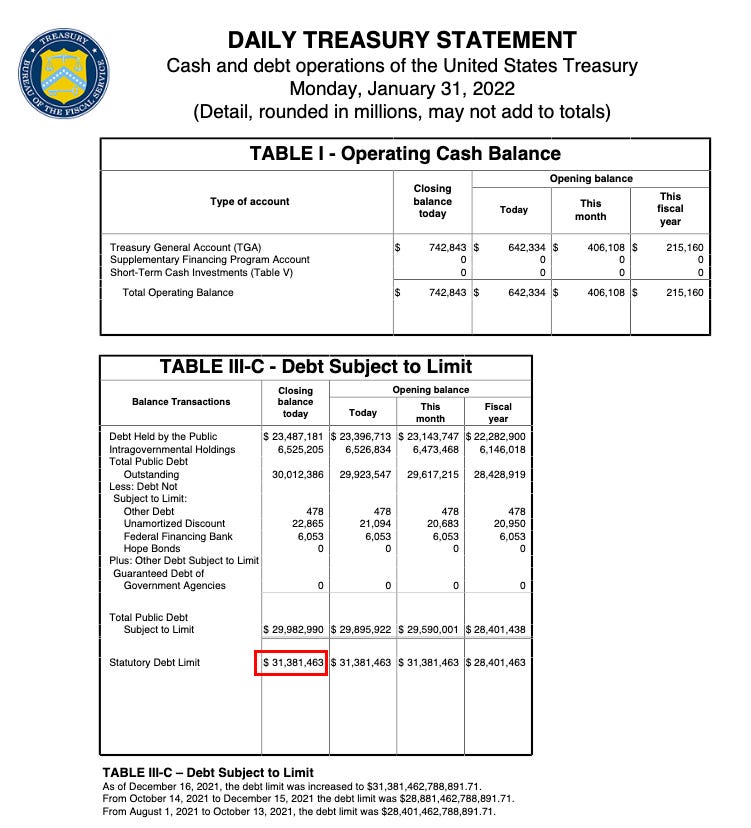

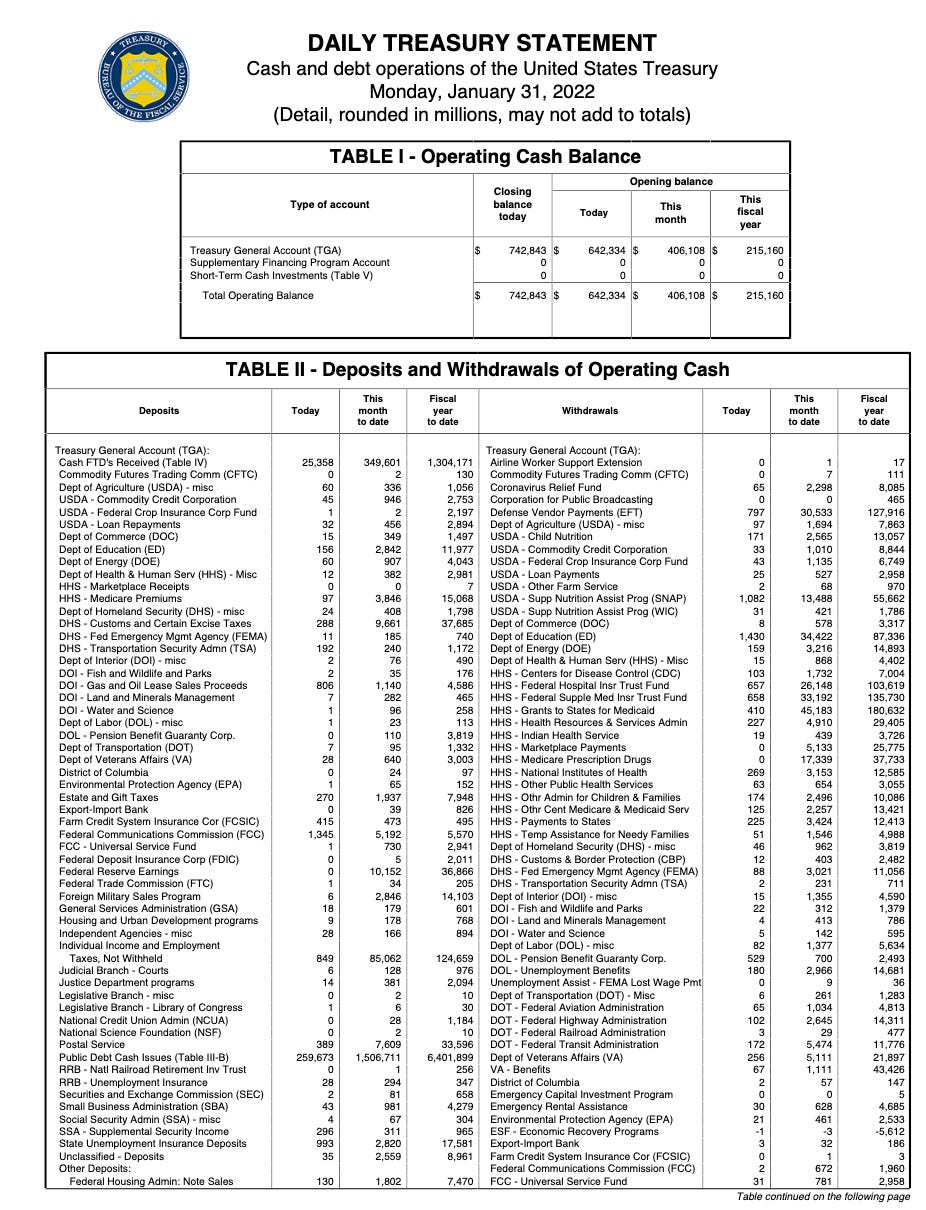

US Debt Tops $30 Trillion

https://fsapps.fiscal.treasury.gov/dts/files/22013100.pdf

The U.S. national debt topped $30 trillion according to Treasury Department data.

National debt grew significantly during the COVID-19 pandemic, increasing by $7 trillion since the end of 2019.

Almost $8 trillion of the total $30 trillion in national debt is owed to foreign investors, with Japan and China the top creditors, which must be repaid with interest.

U.S. debt has skyrocketed in past decades, beginning with the Great Recession of 2008 and exacerbated by the COVID-19 pandemic. The national debt was $9.2 trillion in December 2007, before the financial crisis of 2008.

“Hitting the $30 trillion mark is clearly an important milestone in our dangerous fiscal trajectory. For many years before Covid, America had an unsustainable structural fiscal path because the programs we’ve designed are not sufficiently funded by the revenue we take in. ” Michael Peterson, head of the Peter G. Peterson Foundation

MEPs vote against European Bitcoin ban

Monday, 14th March 2022: Proof of work cryptocurrencies like Bitcoin are safe in Europe for now, but plans to ban environmentally-damaging mining could return.

A watered-down version of the legislation will continue to move forward though, paving the way for possible controversy in future years.

On Monday the European Parliament’s economic and monetary affairs committee voted 30-23 not to take forward an amended version of MiCA requiring all currency providers to submit detailed proposals about how they would comply with environmental sustainability standards.

This would have been virtually impossible for PoW cryptocurrencies like Bitcoin which rely on highly energy-intensive mining processes to generate and verify transactions.

Instead, a more mild version of the bill will continue its legislative journey. It states that by January 1 2025, the European Commission shall present a new proposal “with a view to including in the EU sustainable finance taxonomy any crypto-asset mining activities that contribute substantially to climate change mitigation and adaption”. While this could eventually lead to bans on PoW currencies, it leaves much more room for further debate and amendments.

Part of the European Union’s Digital Finance Strategy, the Markets in Crypto Assets (MiCA) legislation had previously been amended to remove the controversial passage, but a new amendment was added over the weekend which saw it brought back. However, lawmakers decided against backing this change, which had drawn predictable criticism from the cryptocurrency community.

US Bank Exposure to Russian Sanctions

U.S. banks are owed a whopping $14.7 billion by Russian entities, with Citigroup having $10 billion in total exposure to Russia. Citi said it was “continuing previously announced efforts to exit our consumer banking business in Russia” and operating its business in the country on a limited basis.

Goldman Sachs said it was also winding down exposure to Russian businesses this month. The bank had credit exposure of $650 million in Russia as of December 2021 but said losses from the divestiture should be “immaterial.”

JPMorgan Chase, which has roughly 160 staff in Moscow, also said it was cutting ties to Russian businesses in compliance with regulatory requirements, noting that its exposure to the country was “limited.” JPMorgan—the largest bank in the U.S. in terms of total assets—didn’t list Russia as one of the top 20 countries in which it has the most exposure in its November 2021 quarterly SEC filing.

The investment management firm Pimco also held at least $1.5 billion of Russian sovereign debt, plus an additional $1.1 billion in exposure to Russia’s credit default swap market, before the war. Other investment managers with significant Russian debt exposure include Janus Henderson, Ashmore, and Western Asset, according to Morningstar.

European exposure

European banks have revealed even more substantial ties to Russian businesses in the weeks since the invasion of Ukraine. Banks around Europe held a total of $84 billion in claims from Russian entities as of late February, according to the Bank for International Settlements.

The French bank Société Générale had one of the largest ties to Russian businesses, with $21 billion in total exposure as of the end of last year.

In a March 3 statement detailing its work to cut its Russian ties, the bank said that it “complies rigorously with legislation in force and diligently applies all necessary measures to strictly observe international sanctions as soon as they become public.”

BNP Paribas is dealing with $3 billion in Russia exposure, while Deutsche Bank said in a statement last week that it has “limited” dealings with Russian businesses, involving gross loan exposure of $1.5 billion.

Credit Suisse detailed $1.7 billion in exposure to Russia-linked entities. The Swiss bank was caught trying to shred evidence of its loans to Russian oligarchs backed by superyachts and private jets earlier this week.

Despite the losses, European Central Bank vice president Luis de Guindos said the financial system around Europe is not in danger of a liquidity crisis as damage to Europe’s banks remains limited.

“Russia is important in terms of energy markets, in terms of commodity prices, but in terms of the exposure of the financial sector, of the European financial sector, Russia is not very relevant,” de Guindos told CNN

Chernobyl Exclusion Zone |

Analysis: In the greater picture of the Kyiv offensive, the capture of Chernobyl can be considered a waypoint for Russian troops advancing towards Kyiv. Ben Hodges, former commanding general of the United States Army Europe, stated that the exclusion zone was "important because of where it sits... If Russian forces were attacking Kyiv from the north, Chernobyl is right there on the way."

The Exclusion Zone is important for containing fallout from the Chernobyl nuclear disaster of 1986; as such, Ukrainian interior affairs advisor Anton Herashchenko said that "if the occupiers' artillery strikes hit the nuclear waste storage facility, radioactive dust may cover the territories of Ukraine, Belarus and the EU countries

The Department of Defense’s Cooperative Threat Reduction Program

- Biological Threat Reduction Program Activities in Ukraine

FACTSHEET

The Biological Threat Reduction Program (BTRP), part of the Department of

Defense’s Cooperative Threat Reduction (CTR) Program, is implemented by the Defense Threat Reduction Agency (DTRA).

Since 2005, BTRP has partnered with the Government of Ukraine to support peaceful and safe biological detection and diagnostic capabilities and to reduce the threats posed by pathogens.

The Ukraine Embassy says the BTRP is designed to counter outbreaks of the world's most dangerous infections.

Through the BTRP, the U.S. has invested approximately $200 million in Ukraine since 2005, supporting over 40 Ukrainian labs, health facilities and diagnostic sites, according to the DOD.

"DoD's CTR Program began its biological work with Ukraine to reduce the risk posed by the former Soviet Union's illegal biological weapons program, which left Soviet successor states with unsecured biological materials after the fall of the USSR," the DOD states in a fact sheet about the CTR program.

The United Nations has said it is not aware of any biological weapons programs in Ukrain

Zhao claims that the U.S. spent $200 million funding bio-labs and questioned what kind of research was being conducted.

The Chinese Foreign Ministry urged American leaders to provide "thorough clarification" regarding any biological military activities.

"This will help restore the international community's confidence in the U.S. fulfillment of its international obligations and strengthen global biosecurity," the spokesperson, Zhao Lijian, said.

Russia to make external debt payments in roubles

Russia has threatened to pay international bondholders in roubles rather than dollars as a tool to avoid defaults while capital controls remain in place, just days before a key interest payment on its external debt comes due.

The new requirement, which comes three weeks after Washington and Brussels approved sweeping measures targeting Moscow’s financial sector, applies to amounts in excess of 10 million rubles ($81,900) per month. Payments will be considered executed if they are carried out in rubles at the Central Bank of Russia’s official rate.

Anton Siluanov, Russia’s finance minister, said on Sunday that it was “absolutely fair” the country would make all of its sovereign debt payments in roubles until western sanctions that he claimed have frozen $300bn of the country’s reserves were lifted.

Moscow is scheduled to make a combined $117mn in interest payments this Wednesday on two dollar-denominated bonds, according to JPMorgan. Neither bond’s contracts gives Russia the option of paying in roubles, according to the Wall Street bank.

The new requirement, which comes three weeks after Washington and Brussels approved sweeping measures targeting Moscow’s financial sector, applies to amounts in excess of 10 million rubles ($81,900) per month. Payments will be considered executed if they are carried out in rubles at the Central Bank of Russia’s official rate.

According to the decree, debtors can request a Russian lender to open a special “C” ruble-denominated account in the name of foreign creditors for settlement with local creditors to be paid through Russian depositories.

Earlier this week, International Central Securities Depositories (ICSD) Euroclear and Clearstream stopped settling rouble-denominated transactions. The depository excluded all securities issued by Russian entities from all Triparty transactions, restricting access to the tool traditionally used to make payments to bondholders.

Creditors from Russia and the states that have not joined the sanctions will be able to receive debt payments in rubles or in foreign currency after getting a special permit by the Central Bank